NAIROBI, Kenya — Kenya’s economy is poised for stronger-than-expected performance this year after the World Bank revised its growth projection upward to 4.9pc, citing a sharp recovery in the construction sector that had previously been weakened by last year’s political disruptions.

In its latest assessment released Monday, the Bretton Woods institution upgraded its earlier May forecast of 4.5pc, pointing to renewed activity in building and infrastructure works. The Bank noted that the sector, which had slumped during the 2024 protests, is now showing sustained momentum.

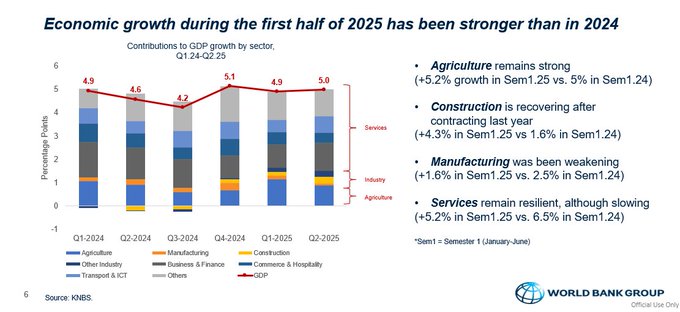

“Signs of recovery are emerging,” the World Bank observed, adding that growth in construction during the first half of 2025 had “offset a slowdown in manufacturing,” giving the overall economy a firmer footing.

Fiscal strains are deepening as public revenues continue to underperform. Public debt has continued to rise, with a large portion of it being domestic debt, increasing risks. #KenyaEconomicUpdate Qimiao Fan, World Bank Division Director

The cautious optimism comes after a difficult 2024, when construction posted 0.1pc growth in the first quarter — a steep fall from 3.0pc in the corresponding period of 2023.

The downturn was reflected in a 12.7pc drop in cement consumption and a 32.4pc plunge in bitumen imports, illustrating suppressed activity in both public and private projects.

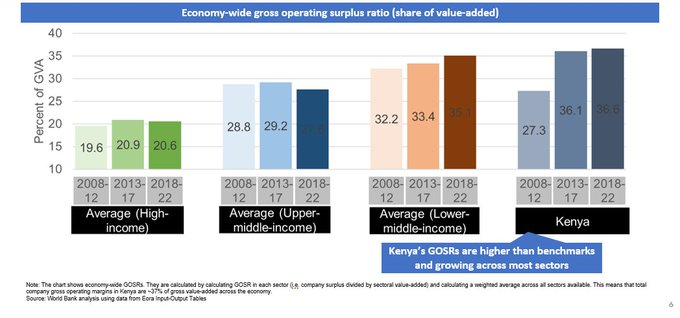

Kenya’s gross operating surpluses have risen over timenow exceeding averages in both high-income and middle-income countries. This signals substantial room to boost competition and unlock greater economic efficiency. #KenyaEconomicUpdate

President William Ruto has maintained that the economy is already expanding faster than external projections, telling Parliament during the State of the Nation Address that Kenya’s current growth rate stands between 5pc and 5.8pc.

Treasury Cabinet Secretary John Mbadi reinforced this estimate, linking anticipated growth above five per cent to fiscal consolidation and restrained public spending.

Ruto added that global financiers shared similar optimism. “Just this week, 14 of the world’s leading financial institutions, including Citigroup, J.P. Morgan, Standard Chartered, and Goldman Sachs, projected that Kenya’s economy will expand by between 5pc and 5.8pc in 2026,” the President said.

Kenya has made important progress in its economic transformation agenda in the past decade, but significant legal and regulatory hurdles continue to impede competition across multiple sectors. #KenyaEconomicUpdate

He attributed their forecasts to declining credit costs, rising exports, improved household spending driven by low inflation, and what he termed a broadly stable macroeconomic environment.

Despite the upbeat projections, the World Bank cautioned that Kenya’s aggressive fiscal consolidation — a key feature of the current administration — could constrain economic activity in the near term.

The institution also flagged the expiry of the African Growth and Opportunity Act (AGOA) in September as a potential risk, though Kenya remains confident that negotiations with President Donald Trump’s administration will secure an extension before year’s end.

The report recommended structural reforms aimed at boosting competition, supporting private investment, and strengthening long-term economic resilience.

Earlier in May, President Ruto’s economic advisor, David Ndii, had warned that construction would continue to decline, arguing that the sector’s earlier boom was fuelled by debt-financed projects that the government could no longer sustain. “The construction boom was debt-financed. Party is over,” Ndii said at the time.

However, the World Bank’s revised projections — combined with the state’s expansive affordable housing programme — suggest that the sector may be regaining traction, offering a renewed engine for national growth over the next two years.

Economic growth during the first half of 2025 has been stronger than in 2024 #KenyaEconomicUpdate

{kind=link}